This guide supports university earnings operations with managing inventory in compliance with Ohio State’s Inventory Policy. It is intended specifically for Earnings Operations that manage their Inventory using a third party system and journals in Workday rather than the Workday Inventory Module.

Inventory Definition and Criteria:

Items meeting both the criteria below are considered Inventory, and must be tracked as such in the Balance Sheet.

- Inventory includes goods held for resale or materials used in producing items for sale.

- Must be part of ongoing operations and owned by Ohio State.

Not inventory: internal-use items (e.g., office supplies), perishables (e.g., food, animal feed), and low-value items.

Policy Considerations:

Inventory Tracking Requirements:

- Must be tracked in a third-party system (not Excel) or in Workday for approved inventory sites.

- Inventory must be counted annually, or through periodic cycle counts.

- Use the average cost method for valuation.

- Monthly reconciliations are required for perpetual inventory systems.

- See the Inventory Policy for full details and requirements.

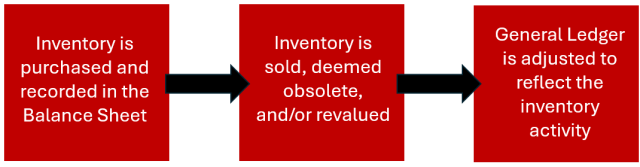

Process

- Inventory is Purchase and Recorded in the Balance Sheet.

- When inventory is purchased, the following Worktags are used on the procurement transaction:

- Cost Center and Balancing Unit for the earnings operation

- Appropriate Earnings Fund.

- ET131 to ensure the purchase posts to the Inventories ledger account (15000)

- A stockable Spend Category (see key reports)

- When inventory is purchased, the following Worktags are used on the procurement transaction:

- Inventory is sold, deemed obsolete, and/or revalued.

- During the course of normal business, inventory items are sold, may be deemed obsolete, or have their valuation changed. This activity is then reflected in the General Ledger via Cost Center Journals (see step 3).

- General Ledger is adjusted to reflect the inventory activity.

When using a third-party system (not Workday) to manage your Inventory, you will need to complete Cost Center Journals when selling or adjusting your inventory. Below you will find high level information about the required entries. You may also wish to review the Inventory Accounting Guide for Earnings Operations hosted on Accounting’s website.

Adjusting Inventory:

The following spend categories should be used in your Cost Center Journal when adjusting inventory balances.

| Spend Category | Description |

|---|---|

| SC10744: Inventory Shrinkage | To reduce or increase the value of inventory when your on-hand quantity is different than the expected amount. |

| SC11039: Inventory Obsolete | To fully reduce the value of inventory due to obsolescence. |

| SC11041: Inventory Spoilage | To fully reduce the value of inventory for reasons other than obsolescence, such as damage or destruction. |

| SC11040: Inventory Cost Adjustment | To reduce or increase inventory due to changes in average cost, or other value adjustments. |

Roles and Responsibilities Associated with Non-Workday Managed Inventory

| Role | Responsibility |

|---|---|

| Finance Director | Ensure independent inventory counts and internal controls are in place. |

| Inventory/Earnings Operation Manager | Maintain inventory balances, apply correct Worktags, and reconcile with accounting. |

| Cost Center Manager/Accountant | Record inventory transactions in the balance sheet and assist with reconciliations. |

Key Reports Associated with Non-Workday Managed Inventory

| Report Name | Purpose |

|---|---|

| Managerial Balance Sheet | View inventory balances and activity in your inventories ledger account (15000: Inventories). |

| Find Journal Lines – OSU | Review detailed journal line information. |

| Find Supplier Invoice Details – OSU | Verify purchase amounts and check for proper expenditure treatment (ET131). |

| Spend Categories – FDM Values | Use this report to determine which Spend Categories are stockable by referring to the “Spend Category is Stockable” column. |

Key Training, Job Aids, and Resources

| Inventory for Earnings Operations (BuckeyeLearn) | Explore the fundamentals of inventory management in earnings operations, including journal entries for tracking, adjustments, and sales, as well as helpful Workday reports. |

| Overhead (BuckeyeLearn) | Explains how Cost of Sales impacts overhead charges for Earnings Operations. |

| Cost of Sales (BuckeyeLearn) | Explains what items qualify as Cost of Sales, and how to ensure expenses are properly classified as Cost of Sales in the General Ledger. |

| Inventory Accounting Guide for Earnings Operations: | Reference guide on the accounting entries used to track inventory, and the Workday Business Processes that originate the accounting entries (when applicable). This guide may be useful when completing Cost Center Journals to ensure the proper ledger accounts are used, and which debits and credits will increase or decrease balances. |

Notable Information

- Departments should consider the administrative costs associated with managing Inventory to ensure financial viability before undertaking new activities.

- Inventory must be associated with an approved Earnings Operation and tracked using the appropriate Worktags.

- Inventory that is not managed in Workday’s Inventory Module must be tracked in the General Ledger via Cost Center Journals.

- Inventory managed externally should be reconciled with the General Ledger at least monthly.

- Unlike other expenses, Inventory is recognized as an expense in the General Ledger at the time of sale, prior to sale Inventory is recognized as an asset.

Selling Inventory

- When selling inventory a Cost Center Journal is needed to reduce your inventory balance, and book the expense to your income statement.

- Debit ledger account 61020: Cost of Sales to post the expense

- Credit ledger account 15000: Inventories to reduce your inventory balance

- Use the current average cost of items sold to ensure accuracy, this should be tracked in your inventory software.

- Example: Selling 100 widgets at an average cost of $25.67 requires a $2,567 reduction in inventory and a matching cost of sales entry.